Futures Market: Overnight, LME copper opened at $9,178/mt, initially dipping to $9,155/mt before climbing steadily, peaking near the session's end at $9,292/mt, and finally closing at $9,291/mt, up 0.27%. Trading volume reached 20,000 lots, and open interest stood at 298,000 lots. Overnight, the most-traded SHFE copper 2503 contract opened at 75,380 yuan/mt, initially dipping to 75,350 yuan/mt before fluctuating upward, peaking near the session's end at 75,740 yuan/mt, and finally closing at 75,700 yuan/mt, up 0.08%. Trading volume reached 21,000 lots, and open interest stood at 160,000 lots.

【SMM Copper Morning Brief】News: (1) On his first day in office, Trump signed over 40 presidential executive orders; Rubio was sworn in as US Secretary of State.

(2) The market struggled with uncertainties surrounding Trump's tariff policies, with the US dollar index rising initially and then falling.

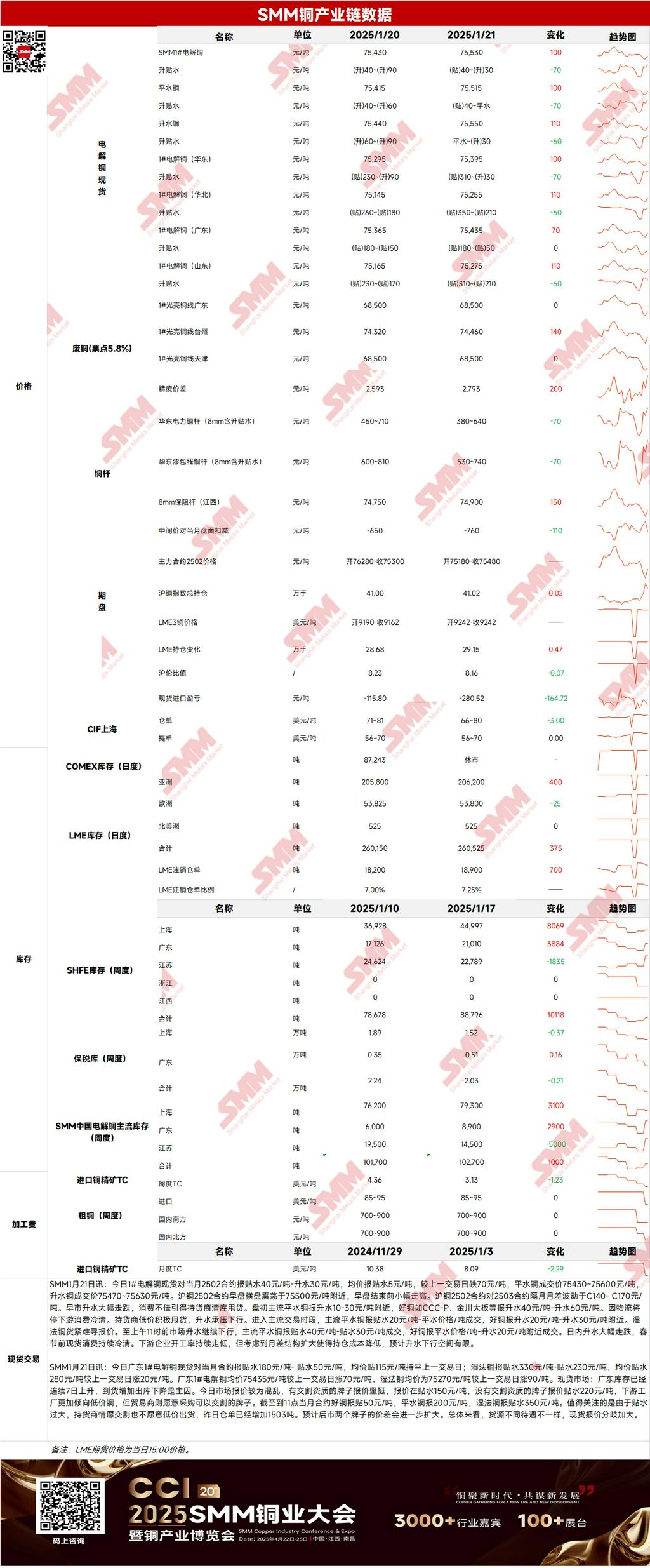

Spot Market: (1) Shanghai: On January 21, #1 copper cathode spot prices against the front-month 2502 contract were quoted at a discount of 40 yuan/mt to a premium of 30 yuan/mt, with an average price at a discount of 5 yuan/mt, down 70 yuan/mt from the previous trading day. Spot premiums dropped significantly yesterday as spot consumption remained sluggish ahead of the Chinese New Year. Downstream operating rates continued to decline, but considering the widening price spread between futures contracts, which reduced holding costs, the downside room for premiums is expected to be limited.

(2) Guangdong: On January 21, #1 copper cathode spot prices against the front-month contract were quoted at a discount of 180 yuan/mt to a discount of 50 yuan/mt, with an average price at a discount of 115 yuan/mt, flat from the previous trading day. Overall, different sources of goods received varying treatments, leading to increased divergence in spot quotations.

(3) Imported Copper: On January 21, warehouse warrant prices were $66-80/mt, QP February, with an average price down $3/mt from the previous trading day; B/L prices were $56-70/mt, QP February, with the average price flat from the previous trading day; EQ copper (CIF B/L) was quoted at $6-20/mt, QP February, with the average price flat from the previous trading day. Quotations referenced cargoes arriving in late January and early February. Yesterday, the SHFE/LME price ratio against the SHFE copper 2502 contract was around -580 yuan/mt, LME copper 3M-Feb was at C$68.67/mt, and the 2502-month date to 2503-month date was at C$35/mt. The import window remained firmly closed yesterday. Pre-holiday downstream demand gradually weakened, with scattered offers for March QP cargoes in the market, but overall transactions were poor.

(4) Secondary Copper: On January 21, secondary copper raw material prices remained unchanged WoW. Guangdong bare bright copper prices were 68,400-68,600 yuan/mt, flat from the previous trading day. The price difference between primary metal and scrap was 2,793 yuan/mt, up 200 yuan/mt WoW. The price difference between primary and secondary copper rods was 1,270 yuan/mt. According to the SMM survey, secondary copper rod plants indicated that most logistics operations had ceased as of today, with raw material procurement and customer shipments postponed until after the holiday.

(5) Inventory: On January 21, LME copper cathode inventories increased by 375 mt to 260,525 mt; SHFE warehouse warrant inventories increased by 1,468 mt to 16,917 mt.

Prices: Macro side, Trump provided no specific details regarding the imposition of universal tariffs or additional tax surcharges on major trading partners. However, he hinted at the possibility of imposing tariffs on Canadian and Mexican goods as early as February 1. The market struggled with uncertainties surrounding Trump's tariff policies, with the US dollar index rising initially and then falling, and copper prices following a similar pattern. Fundamentals side, as the Chinese New Year break approached, logistics operations ceased, and enterprises gradually entered holiday mode. New orders in the market were limited, demand continued to weaken, and spot premiums maintained a downward trend. In terms of prices, with tariff policies still unclear, the US dollar is expected to fluctuate at its current high level, making further increases unlikely. Copper prices are expected to fluctuate rangebound today.

》Click to View the SMM Metal Database

【The above information is based on market data and comprehensive assessments by the SMM research team. The information provided herein is for reference only and does not constitute direct investment research advice. Clients should make prudent decisions and not substitute this information for independent judgment. Any decisions made by clients are unrelated to SMM.】